24. Debiased ML for Partially Linear IV Model in Python#

24.1. Double/Debiased ML for Partially Linear IV Model#

References:

https://arxiv.org/abs/1608.00060

https://www.amazon.com/Business-Data-Science-Combining-Accelerate/dp/1260452778

The code is based on the book.

24.2. Partially Linear IV Model#

We consider the partially linear structural equation model:

Note that this model is not a regression model unless \(Z=D\). The model is a canonical model in causal inference, going back to P. Wright’s work on IV methods for estimaing demand/supply equations, with the modern difference being that \(g_0\) and \(m_0\) are nonlinear, potentially complicated functions of high-dimensional \(X\).

The idea of this model is that there is a structural or causal relation between \(Y\) and \(D\), captured by \(\theta_0\), and \(g_0(X) + \zeta\) is the stochastic error, partly explained by covariates \(X\). \(V\) and \(\zeta\) are stochastic errors that are not explained by \(X\). Since \(Y\) and \(D\) are jointly determined, we need an external factor, commonly referred to as an instrument, \(Z\) to create exogenous variation in \(D\). Note that \(Z\) should affect \(D\). The \(X\) here serve again as confounding factors, so we can think of variation in \(Z\) as being exogenous only conditional on \(X\).

The causal DAG this model corresponds to is given by:

where \(L\) is the latent confounder affecting both \(Y\) and \(D\), but not \(Z\).

Example

A simple contextual example is from biostatistics, where \(Y\) is a health outcome and \(D\) is indicator of smoking. Thus, \(\theta_0\) is captures the effect of smoking on health. Health outcome \(Y\) and smoking behavior \(D\) are treated as being jointly determined. \(X\) represents patient characteristics, and \(Z\) could be a doctor’s advice not to smoke (or another behavioral treatment) that may affect the outcome \(Y\) only through shifting the behavior \(D\), conditional on characteristics \(X\).

PLIVM in Residualized Form

The PLIV model above can be rewritten in the following residualized form:

where

The tilded variables above represent original variables after taking out or “partialling out” the effect of \(X\). Note that \(\theta_0\) is identified from this equation if \(V\) and \(U\) have non-zero correlation, which automatically means that \(U\) and \(V\) must have non-zero variation.

DML for PLIV Model

Given identification, DML proceeds as follows

Compute the estimates \(\hat \ell_0\), \(\hat r_0\), and \(\hat m_0\) , which amounts to solving the three problems of predicting \(Y\), \(D\), and \(Z\) using \(X\), using any generic ML method, giving us estimated residuals

The estimates should be of a cross-validated form, as detailed in the algorithm below.

Estimate \(\theta_0\) by the the intstrumental variable regression of \(\tilde Y\) on \(\tilde D\) using \(\tilde Z\) as an instrument. Use the conventional inference for the IV regression estimator, ignoring the estimation error in these residuals.

The reason we work with this residualized form is that it eliminates the bias arising when solving the prediction problem in stage 1. The role of cross-validation is to avoid another source of bias due to potential overfitting.

The estimator is adaptive, in the sense that the first stage estimation errors do not affect the second stage errors.

# Import packages

import pandas as pd

import numpy as np

import pyreadr

import os

from urllib.request import urlopen

from sklearn import preprocessing

import patsy

from numpy import loadtxt

from keras.models import Sequential

from keras.layers import Dense

import hdmpy

import numpy as np

import random

import statsmodels.api as sm

import matplotlib.pyplot as plt

import numpy as np

from matplotlib import colors

from sklearn.tree import DecisionTreeRegressor

from sklearn.ensemble import RandomForestRegressor

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.linear_model import LassoCV

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import RidgeCV, ElasticNetCV

from sklearn.linear_model import LinearRegression

from sklearn import linear_model

import itertools

from pandas.api.types import is_string_dtype

from pandas.api.types import is_numeric_dtype

from pandas.api.types import is_categorical_dtype

from itertools import compress

import statsmodels.api as sm

import statsmodels.formula.api as smf

from sklearn.feature_selection import SelectFromModel

from statsmodels.tools import add_constant

from sklearn.linear_model import ElasticNet

import hdmpy

from scipy.stats import chi2

from sklearn.model_selection import KFold

import warnings

warnings.filterwarnings('ignore')

from linearmodels.iv import IV2SLS

import numpy as np

from statsmodels.api import add_constant

from linearmodels.datasets import mroz

link="https://raw.githubusercontent.com/d2cml-ai/14.388_py/main/data/ajr.RData"

response = urlopen(link)

content = response.read()

fhandle = open( 'ajr.Rdata', 'wb')

fhandle.write(content)

fhandle.close()

result = pyreadr.read_r("ajr.Rdata")

os.remove("ajr.Rdata")

# Extracting the data frame from rdata_read

AJR = result[ 'AJR' ]

AJR.shape

(64, 11)

def DML2_for_PLIVM(x, d, z , y, dreg, yreg, zreg, nfold = 2 ):

kf = KFold(n_splits = nfold, shuffle=True) #Here we use kfold to generate kfolds

I = np.arange(0, len(d)) #To have a id vector from data

train_id, test_id = [], [] #arrays to store kfold's ids

#generate and store kfold's id

for kfold_index in kf.split(I):

train_id.append(kfold_index[0])

test_id.append(kfold_index[1])

# Create array to save errors

dtil = np.zeros( len(z) ).reshape( len(z) , 1 )

ytil = np.zeros( len(z) ).reshape( len(z) , 1 )

ztil = np.zeros( len(z) ).reshape( len(z) , 1 )

total_modelos = []

total_sample = 0

# loop to save results

for b in range(0,len(train_id)):

# Lasso regression, excluding folds selected

dfit = dreg(x[train_id[b],], d[train_id[b],])

zfit = zreg(x[train_id[b],], z[train_id[b],])

yfit = yreg(x[train_id[b],], y[train_id[b],])

# predict estimates using the

dhat = dfit.predict( x[test_id[b],] )

zhat = zfit.predict( x[test_id[b],] )

yhat = yfit.predict( x[test_id[b],] )

# save errors

dtil[test_id[b]] = d[test_id[b],] - dhat.reshape( -1 , 1 )

ztil[test_id[b]] = z[test_id[b],] - zhat.reshape( -1 , 1 )

ytil[test_id[b]] = y[test_id[b],] - yhat.reshape( -1 , 1 )

total_modelos.append( dfit )

print(b, " ")

# Create dataframe

ivfit = IV2SLS( exog = None , endog = dtil , dependent = ytil , instruments = ztil ).fit( cov_type = 'unadjusted' ) ## unadjusted == homocedastick

# OLS clustering at the County level

coef_est = ivfit.params[0]

se = ivfit.std_errors[0]

print( f"\n Coefficient (se) = {coef_est} ({se})" )

Final_result = { 'coef_est' : coef_est , 'se' : se , 'dtil' : dtil , 'ytil' : ytil , 'ztil' : ztil , 'modelos' : total_modelos }

return Final_result

24.3. Emprical Example: Acemoglu, Jonsohn, Robinson (AER).#

Y is log GDP;

D is a measure of Protection from Expropriation, a proxy for quality of insitutions;

Z is the log of Settler’s mortality;

W are geographical variables (latitude, latitude squared, continent dummies as well as interactions)

y = AJR[['GDP']].to_numpy()

d = AJR[['Exprop']].to_numpy()

z = AJR[['logMort']].to_numpy()

xraw_formula = " GDP ~ Latitude+ Africa+Asia + Namer + Samer"

x_formula = " GDP ~ -1 + ( Latitude + Latitude2 + Africa + Asia + Namer + Samer ) ** 2"

y_model, xraw_dframe = patsy.dmatrices( xraw_formula, AJR , return_type='matrix')

y_model, x_dframe = patsy.dmatrices( x_formula, AJR , return_type='matrix')

xraw = np.asarray( xraw_dframe , dtype = np.float64 )

x = np.asarray( x_dframe , dtype = np.float64)

Information from random Forest link1, link2

y_model, x_dframe2 = patsy.dmatrices( x_formula, AJR , return_type='dataframe')

x_dframe2

| Latitude | Latitude2 | Africa | Asia | Namer | Samer | Latitude:Latitude2 | Latitude:Africa | Latitude:Asia | Latitude:Namer | ... | Latitude2:Africa | Latitude2:Asia | Latitude2:Namer | Latitude2:Samer | Africa:Asia | Africa:Namer | Africa:Samer | Asia:Namer | Asia:Samer | Namer:Samer | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.3111 | 0.096783 | 1.0 | 0.0 | 0.0 | 0.0 | 0.030109 | 0.3111 | 0.0000 | 0.0000 | ... | 0.096783 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 1 | 0.1367 | 0.018687 | 1.0 | 0.0 | 0.0 | 0.0 | 0.002554 | 0.1367 | 0.0000 | 0.0000 | ... | 0.018687 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 2 | 0.3778 | 0.142733 | 0.0 | 0.0 | 0.0 | 1.0 | 0.053924 | 0.0000 | 0.0000 | 0.0000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.142733 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 3 | 0.3000 | 0.090000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.027000 | 0.0000 | 0.0000 | 0.0000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 4 | 0.2683 | 0.071985 | 0.0 | 0.0 | 1.0 | 0.0 | 0.019314 | 0.0000 | 0.0000 | 0.2683 | ... | 0.000000 | 0.000000 | 0.071985 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 59 | 0.3667 | 0.134469 | 0.0 | 0.0 | 0.0 | 1.0 | 0.049310 | 0.0000 | 0.0000 | 0.0000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.134469 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 60 | 0.4222 | 0.178253 | 0.0 | 0.0 | 1.0 | 0.0 | 0.075258 | 0.0000 | 0.0000 | 0.4222 | ... | 0.000000 | 0.000000 | 0.178253 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 61 | 0.0889 | 0.007903 | 0.0 | 0.0 | 0.0 | 1.0 | 0.000703 | 0.0000 | 0.0000 | 0.0000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.007903 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 62 | 0.1778 | 0.031613 | 0.0 | 1.0 | 0.0 | 0.0 | 0.005621 | 0.0000 | 0.1778 | 0.0000 | ... | 0.000000 | 0.031613 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 63 | 0.0000 | 0.000000 | 1.0 | 0.0 | 0.0 | 0.0 | 0.000000 | 0.0000 | 0.0000 | 0.0000 | ... | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

64 rows × 21 columns

def dreg( x_1 , d_1 ):

if d_1 is not None and ( d_1.dtype != str ):

mtry1 = max( [ np.round( ( x_1.shape[ 1 ]/3 ) ) , 1 ] ).astype(int)

else:

mtry1 = np.round( np.sqrt( x_1.shape[ 1 ] ) ).astype(int)

if d_1 is not None and ( d_1.dtype != str ):

nodesize1 = 5

else:

nodesize1 = 1

result = RandomForestRegressor( random_state = 0 , n_estimators = 500 , max_features = mtry1 , n_jobs = 4 , min_samples_leaf = nodesize1 ).fit( x_1 , d_1 )

return result

def yreg( x_1 , y_1 ):

if y_1 is not None and ( y_1.dtype != str ):

mtry1 = max( [ np.round( ( x_1.shape[ 1 ]/3 ) ) , 1 ] ).astype(int)

else:

mtry1 = np.round( np.sqrt( x_1.shape[ 1 ] ) ).astype(int)

if y_1 is not None and ( y_1.dtype != str ):

nodesize1 = 5

else:

nodesize1 = 1

result = RandomForestRegressor( random_state = 0 , n_estimators = 500 , max_features = mtry1 , n_jobs = 4 , min_samples_leaf = nodesize1 ).fit( x_1, y_1 )

return result

def zreg( x_1 , z_1 ):

if z_1 is not None and ( z_1.dtype != str ):

mtry1 = max( [ np.round( ( x_1.shape[ 1 ]/3 ) ) , 1 ] ).astype(int)

else:

mtry1 = np.round( np.sqrt( x_1.shape[ 1 ] ) ).astype(int)

if z_1 is not None and ( z_1.dtype != str ):

nodesize1 = 5

else:

nodesize1 = 1

result = RandomForestRegressor( random_state = 0 , n_estimators = 500 , max_features = mtry1 , n_jobs = 4 , min_samples_leaf = nodesize1 ).fit( x_1, z_1 )

return result

print( "\n DML with Post-Lasso \n" )

DML with Post-Lasso

DML2_RF = DML2_for_PLIVM(xraw, d, z, y, dreg, yreg, zreg, nfold=20)

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

Coefficient (se) = 0.8113768412168717 (0.25866023849580644)

class rlasso_sklearn:

def __init__(self, post ):

self.post = post

def fit( self, X, Y ):

self.X = X

self.Y = Y

# Standarization of X and Y

self.rlasso_model = hdmpy.rlasso( X , Y , post = self.post )

return self

def predict( self , X_1 ):

self.X_1 = X_1

beta = self.rlasso_model.est['coefficients'].to_numpy()

if beta.sum() == 0:

prediction = np.repeat( self.rlasso_model.est['intercept'] , self.X_1.shape[0] )

else:

prediction = ( add_constant( self.X_1 , has_constant = 'add') @ beta ).flatten()

return prediction

# DML with PostLasso

print( "\n DML with Lasso \n" )

def dreg(x, d):

result = rlasso_sklearn( post = True ).fit( x , d )

return result

def yreg(x,y):

result = rlasso_sklearn( post = True ).fit( x , y )

return result

def zreg(x,z):

result = rlasso_sklearn( post = True ).fit( x , z )

return result

DML with Lasso

DML2_lasso = DML2_for_PLIVM(x, d, z, y, dreg, yreg, zreg, nfold = 20 )

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

Coefficient (se) = 0.7092468711866841 (0.1611789001019162)

# Compare Forest vs Lasso

comp_tab_numpy = np.zeros( ( 3 , 2 ) )

comp_tab_numpy[ 0 , : ] = [ np.sqrt( np.mean( DML2_RF['ytil'] ** 2 ) ) , np.sqrt( np.mean( DML2_lasso['ytil'] ** 2 ) ) ]

comp_tab_numpy[ 1 , : ] = [ np.sqrt( np.mean( DML2_RF['dtil'] ** 2 ) ) , np.sqrt( np.mean( DML2_lasso['dtil'] ** 2 ) ) ]

comp_tab_numpy[ 2 , : ] = [ np.sqrt( np.mean( DML2_RF['ztil'] ** 2 ) ) , np.sqrt( np.mean( DML2_lasso['ztil'] ** 2 ) ) ]

comp_tab = pd.DataFrame( comp_tab_numpy , columns = [ 'RF' ,'LASSO' ] , index = [ "RMSE for Y:", "RMSE for D:", "RMSE for Z:" ] )

comp_tab

| RF | LASSO | |

|---|---|---|

| RMSE for Y: | 0.798088 | 0.928451 |

| RMSE for D: | 1.326933 | 1.595742 |

| RMSE for Z: | 0.946177 | 1.053832 |

24.4. Examine if we have weak instruments#

sm.OLS( DML2_lasso[ 'dtil' ] , DML2_lasso[ 'ztil' ] ).fit( cov_type = 'HC1', use_t = True ).summary()

| Dep. Variable: | y | R-squared (uncentered): | 0.173 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared (uncentered): | 0.160 |

| Method: | Least Squares | F-statistic: | 9.184 |

| Date: | Tue, 26 Jul 2022 | Prob (F-statistic): | 0.00354 |

| Time: | 00:33:58 | Log-Likelihood: | -114.65 |

| No. Observations: | 64 | AIC: | 231.3 |

| Df Residuals: | 63 | BIC: | 233.5 |

| Df Model: | 1 | ||

| Covariance Type: | HC1 |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| x1 | -0.6295 | 0.208 | -3.031 | 0.004 | -1.045 | -0.214 |

| Omnibus: | 1.025 | Durbin-Watson: | 1.701 |

|---|---|---|---|

| Prob(Omnibus): | 0.599 | Jarque-Bera (JB): | 0.926 |

| Skew: | -0.047 | Prob(JB): | 0.630 |

| Kurtosis: | 2.418 | Cond. No. | 1.00 |

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors are heteroscedasticity robust (HC1)

sm.OLS( DML2_RF[ 'dtil' ] , DML2_RF[ 'ztil' ] ).fit( cov_type = 'HC1', use_t = True ).summary()

| Dep. Variable: | y | R-squared (uncentered): | 0.087 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared (uncentered): | 0.073 |

| Method: | Least Squares | F-statistic: | 4.537 |

| Date: | Tue, 26 Jul 2022 | Prob (F-statistic): | 0.0371 |

| Time: | 00:34:00 | Log-Likelihood: | -105.99 |

| No. Observations: | 64 | AIC: | 214.0 |

| Df Residuals: | 63 | BIC: | 216.1 |

| Df Model: | 1 | ||

| Covariance Type: | HC1 |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| x1 | -0.4146 | 0.195 | -2.130 | 0.037 | -0.804 | -0.026 |

| Omnibus: | 0.476 | Durbin-Watson: | 1.615 |

|---|---|---|---|

| Prob(Omnibus): | 0.788 | Jarque-Bera (JB): | 0.375 |

| Skew: | 0.183 | Prob(JB): | 0.829 |

| Kurtosis: | 2.919 | Cond. No. | 1.00 |

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors are heteroscedasticity robust (HC1)

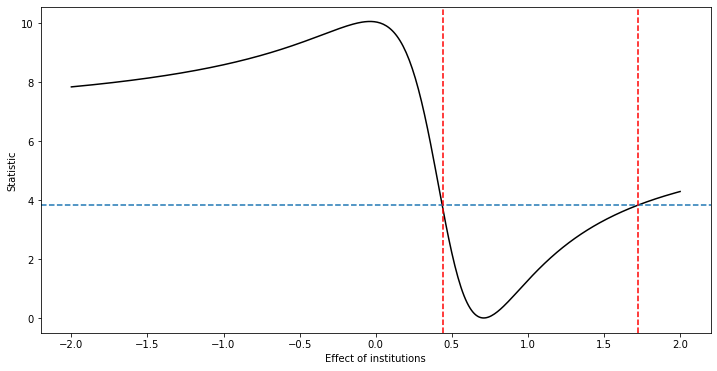

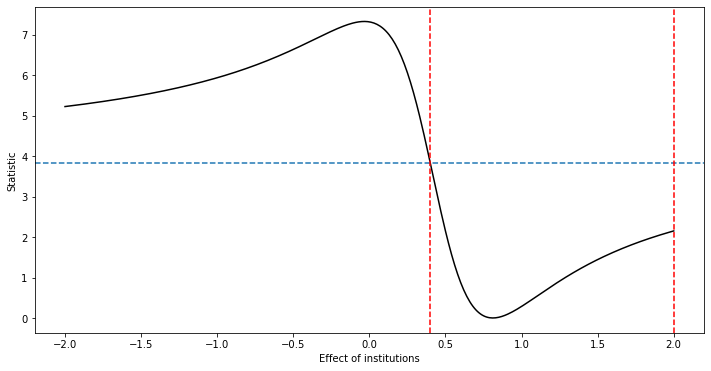

24.5. We do have weak instruments, because t-stats in regression \(\tilde D \sim \tilde Z\) are less than 4 in absolute value#

So let’s carry out DML inference combined with Anderson-Rubin Idea

# DML-AR (DML with Anderson-Rubin)

def DML_AR_PLIV( rY, rD, rZ, grid, alpha = 0.05 ):

n = rY.size

Cstat = np.zeros( grid.size )

for i in range( 0 , grid.size ):

Cstat[ i ] = n * ( ( np.mean( ( rY - grid[ i ] * rD ) * rZ ) ) ** 2 ) / np.var( ( rY - grid[ i ] * rD ) * rZ )

LB = np.min( grid[ Cstat < chi2.ppf( 1 - alpha , 1) ] )

UB = np.max( grid[ Cstat < chi2.ppf( 1 - alpha , 1) ] )

print( "UB =" , UB, "LB =" ,LB)

fig, ax = plt.subplots(figsize=(12, 6))

ax.plot(grid, Cstat, color='black', label='Sine wave' )

ax.axhline( y = chi2.ppf( 1 - 0.05 , 1) , linestyle = "--" )

ax.axvline( x = LB , color = 'red' , linestyle = "--" )

ax.axvline( x = UB , color = 'red' , linestyle = "--" )

ax.set_ylabel('Statistic')

ax.set_xlabel('Effect of institutions')

plt.show()

final_result = { 'UB' : UB , 'LB' : LB }

return final_result

DML_AR_PLIV(rY = DML2_lasso['ytil'], rD= DML2_lasso['dtil'], rZ= DML2_lasso['ztil'],

grid = np.arange( -2, 2.001, 0.01 ) )

UB = 1.7200000000000033 LB = 0.44000000000000217

{'UB': 1.7200000000000033, 'LB': 0.44000000000000217}

DML_AR_PLIV(rY = DML2_RF['ytil'], rD= DML2_RF['dtil'], rZ= DML2_RF['ztil'],

grid = np.arange( -2, 2.001, 0.01 ) )

UB = 2.0000000000000036 LB = 0.40000000000000213

{'UB': 2.0000000000000036, 'LB': 0.40000000000000213}