14. AutoML for wage prediction#

We illustrate how to predict an outcome variable Y in a high-dimensional setting, using the AutoML package H2O that covers the complete pipeline from the raw dataset to the deployable machine learning model. In last few years, AutoML or automated machine learning has become widely popular among data science community. Again, re-analyse the wage prediction problem using data from the U.S. March Supplement of the Current Population Survey (CPS) in 2015.

We can use AutoML as a benchmark and compare it to the methods that we used in the previous notebook where we applied one machine learning method after the other.

# load the H2O package

install.packages("librarian", quiet = T)

librarian::shelf(h2o, tidyverse, quiet = T)

# library(h2o)

Warning message in system("timedatectl", intern = TRUE):

“running command 'timedatectl' had status 1”

# load the data set

data = read_csv("https://github.com/alexanderquispe/14.38_Causal_ML/raw/main/data/wage2015_subsample_inference.csv", show_col_types = F)

# split the data

set.seed(1234)

training <- sample(nrow(data), nrow(data)*(3/4), replace=FALSE)

train <- data[training,]

test <- data[-training,]

# start h2o cluster

h2o.init()

H2O is not running yet, starting it now...

Note: In case of errors look at the following log files:

/tmp/Rtmp04tHzQ/file3c5628322d/h2o_UnknownUser_started_from_r.out

/tmp/Rtmp04tHzQ/file3c7321dc6f/h2o_UnknownUser_started_from_r.err

Starting H2O JVM and connecting: .... Connection successful!

R is connected to the H2O cluster:

H2O cluster uptime: 2 seconds 645 milliseconds

H2O cluster timezone: Etc/UTC

H2O data parsing timezone: UTC

H2O cluster version: 3.36.1.2

H2O cluster version age: 1 month and 23 days

H2O cluster name: H2O_started_from_R_root_tlg556

H2O cluster total nodes: 1

H2O cluster total memory: 3.17 GB

H2O cluster total cores: 2

H2O cluster allowed cores: 2

H2O cluster healthy: TRUE

H2O Connection ip: localhost

H2O Connection port: 54321

H2O Connection proxy: NA

H2O Internal Security: FALSE

R Version: R version 4.2.0 (2022-04-22)

# convert data as h2o type

train_h = as.h2o(train)

test_h = as.h2o(test)

# have a look at the data

h2o.describe(train_h)

|======================================================================| 100%

|======================================================================| 100%

| Label | Type | Missing | Zeros | PosInf | NegInf | Min | Max | Mean | Sigma | Cardinality |

|---|---|---|---|---|---|---|---|---|---|---|

| <chr> | <chr> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> |

| rownames | int | 0 | 0 | 0 | 0 | 10.000000 | 3.264300e+04 | 1.560586e+04 | 9.721144e+03 | NA |

| wage | real | 0 | 0 | 0 | 0 | 3.021978 | 5.288457e+02 | 2.337760e+01 | 2.060944e+01 | NA |

| lwage | real | 0 | 0 | 0 | 0 | 1.105912 | 6.270697e+00 | 2.969673e+00 | 5.721780e-01 | NA |

| sex | int | 0 | 2115 | 0 | 0 | 0.000000 | 1.000000e+00 | 4.523563e-01 | 4.977894e-01 | NA |

| shs | int | 0 | 3770 | 0 | 0 | 0.000000 | 1.000000e+00 | 2.382185e-02 | 1.525136e-01 | NA |

| hsg | int | 0 | 2896 | 0 | 0 | 0.000000 | 1.000000e+00 | 2.501295e-01 | 4.331435e-01 | NA |

| scl | int | 0 | 2795 | 0 | 0 | 0.000000 | 1.000000e+00 | 2.762817e-01 | 4.472157e-01 | NA |

| clg | int | 0 | 2646 | 0 | 0 | 0.000000 | 1.000000e+00 | 3.148628e-01 | 4.645213e-01 | NA |

| ad | int | 0 | 3341 | 0 | 0 | 0.000000 | 1.000000e+00 | 1.349042e-01 | 3.416654e-01 | NA |

| mw | int | 0 | 2872 | 0 | 0 | 0.000000 | 1.000000e+00 | 2.563439e-01 | 4.366704e-01 | NA |

| so | int | 0 | 2707 | 0 | 0 | 0.000000 | 1.000000e+00 | 2.990678e-01 | 4.579089e-01 | NA |

| we | int | 0 | 3034 | 0 | 0 | 0.000000 | 1.000000e+00 | 2.143967e-01 | 4.104563e-01 | NA |

| ne | int | 0 | 2973 | 0 | 0 | 0.000000 | 1.000000e+00 | 2.301916e-01 | 4.210099e-01 | NA |

| exp1 | real | 0 | 49 | 0 | 0 | 0.000000 | 4.700000e+01 | 1.385590e+01 | 1.067133e+01 | NA |

| exp2 | real | 0 | 49 | 0 | 0 | 0.000000 | 2.209000e+01 | 3.058340e+00 | 4.039614e+00 | NA |

| exp3 | real | 0 | 49 | 0 | 0 | 0.000000 | 1.038230e+02 | 8.385453e+00 | 1.465866e+01 | NA |

| exp4 | real | 0 | 49 | 0 | 0 | 0.000000 | 4.879681e+02 | 2.566770e+01 | 5.425545e+01 | NA |

| occ | int | 0 | 0 | 0 | 0 | 10.000000 | 1.000000e+05 | 5.247124e+03 | 1.157852e+04 | NA |

| occ2 | int | 0 | 0 | 0 | 0 | 1.000000 | 2.200000e+01 | 1.168514e+01 | 6.965247e+00 | NA |

| ind | int | 0 | 0 | 0 | 0 | 370.000000 | 1.000000e+05 | 6.605252e+03 | 5.173314e+03 | NA |

| ind2 | int | 0 | 0 | 0 | 0 | 2.000000 | 2.200000e+01 | 1.329777e+01 | 5.691808e+00 | NA |

# define the variables

y = 'lwage'

x = setdiff(names(data), c('wage','occ2', 'ind2'))

# run AutoML for 10 base models and a maximal runtime of 100 seconds

aml = h2o.automl(x=x,y = y,

training_frame = train_h,

leaderboard_frame = test_h,

max_models = 10,

seed = 1,

max_runtime_secs = 100

)

# AutoML Leaderboard

lb = aml@leaderboard

print(lb, n = nrow(lb))

Warning message in .verify_dataxy(training_frame, x, y):

“removing response variable from the explanatory variables”

|======================================================================| 100%

model_id rmse mse

1 StackedEnsemble_AllModels_1_AutoML_1_20220719_171824 0.4669942 0.2180836

2 StackedEnsemble_BestOfFamily_1_AutoML_1_20220719_171824 0.4690110 0.2199713

3 GBM_1_AutoML_1_20220719_171824 0.4709260 0.2217713

4 GBM_2_AutoML_1_20220719_171824 0.4724988 0.2232551

5 GBM_3_AutoML_1_20220719_171824 0.4733774 0.2240862

6 GBM_4_AutoML_1_20220719_171824 0.4740358 0.2247100

7 XGBoost_3_AutoML_1_20220719_171824 0.4791050 0.2295416

8 XRT_1_AutoML_1_20220719_171824 0.4884560 0.2385893

9 DRF_1_AutoML_1_20220719_171824 0.4893117 0.2394260

10 XGBoost_2_AutoML_1_20220719_171824 0.5039629 0.2539786

11 XGBoost_1_AutoML_1_20220719_171824 0.5065185 0.2565610

12 GLM_1_AutoML_1_20220719_171824 0.5159068 0.2661599

mae rmsle mean_residual_deviance

1 0.3479339 0.1176141 0.2180836

2 0.3495583 0.1182146 0.2199713

3 0.3513555 0.1186738 0.2217713

4 0.3540236 0.1189309 0.2232551

5 0.3518737 0.1190304 0.2240862

6 0.3529919 0.1193677 0.2247100

7 0.3582960 0.1207383 0.2295416

8 0.3666487 0.1229990 0.2385893

9 0.3663660 0.1233622 0.2394260

10 0.3757325 0.1267305 0.2539786

11 0.3788916 0.1275746 0.2565610

12 0.3932883 0.1298952 0.2661599

[12 rows x 6 columns]

We see that two Stacked Ensembles are at the top of the leaderboard. Stacked Ensembles often outperform a single model. The out-of-sample (test) MSE of the leading model is given by

aml@leaderboard$mse[1]

mse

1 0.2180836

[1 row x 1 column]

The in-sample performance can be evaluated by

aml@leader

Model Details:

==============

H2ORegressionModel: stackedensemble

Model ID: StackedEnsemble_AllModels_1_AutoML_1_20220719_171824

Number of Base Models: 10

Base Models (count by algorithm type):

drf gbm glm xgboost

2 4 1 3

Metalearner:

Metalearner algorithm: glm

Metalearner cross-validation fold assignment:

Fold assignment scheme: AUTO

Number of folds: 5

Fold column: NULL

Metalearner hyperparameters:

H2ORegressionMetrics: stackedensemble

** Reported on training data. **

MSE: 0.1415518

RMSE: 0.3762337

MAE: 0.2857554

RMSLE: 0.09723326

Mean Residual Deviance : 0.1415518

H2ORegressionMetrics: stackedensemble

** Reported on cross-validation data. **

** 5-fold cross-validation on training data (Metrics computed for combined holdout predictions) **

MSE: 0.219355

RMSE: 0.4683535

MAE: 0.3549446

RMSLE: 0.1199425

Mean Residual Deviance : 0.219355

Cross-Validation Metrics Summary:

mean sd cv_1_valid cv_2_valid cv_3_valid

mae 0.354820 0.014198 0.347980 0.337307 0.369668

mean_residual_deviance 0.219562 0.023919 0.205474 0.190237 0.236612

mse 0.219562 0.023919 0.205474 0.190237 0.236612

null_deviance 253.053390 27.814274 228.977890 252.801100 267.446900

r2 0.327839 0.035450 0.301765 0.389207 0.310545

residual_deviance 169.472760 18.989317 159.447500 154.282040 183.847530

rmse 0.468019 0.025515 0.453292 0.436161 0.486428

rmsle 0.119856 0.006879 0.117210 0.110752 0.122937

cv_4_valid cv_5_valid

mae 0.369248 0.349898

mean_residual_deviance 0.249945 0.215545

mse 0.249945 0.215545

null_deviance 291.623540 224.417530

r2 0.326576 0.311102

residual_deviance 195.456850 154.329910

rmse 0.499945 0.464268

rmsle 0.129307 0.119074

This is in line with our previous results. To understand how the ensemble works, let’s take a peek inside the Stacked Ensemble “All Models” model. The “All Models” ensemble is an ensemble of all of the individual models in the AutoML run. This is often the top performing model on the leaderboard.

model_ids <- as.data.frame(aml@leaderboard$model_id)[,1]

# Get the "All Models" Stacked Ensemble model

se <- h2o.getModel(grep("StackedEnsemble_AllModels", model_ids, value = TRUE)[1])

# Get the Stacked Ensemble metalearner model

metalearner <- se@model$metalearner_model

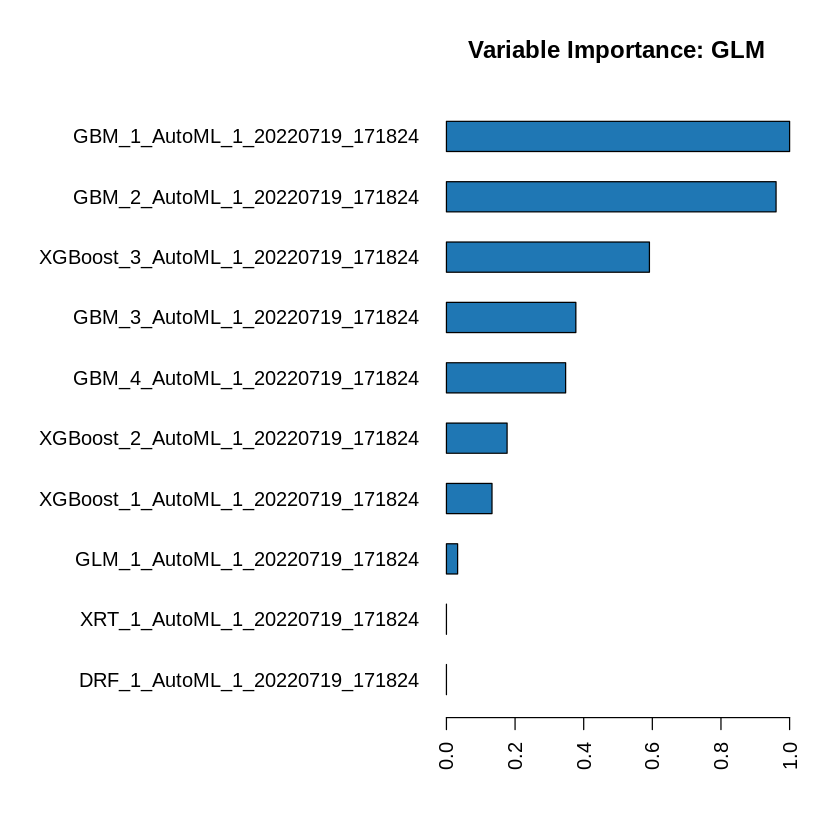

h2o.varimp(metalearner)

| variable | relative_importance | scaled_importance | percentage |

|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> |

| GBM_1_AutoML_1_20220719_171824 | 0.092798688 | 1.00000000 | 0.276345757 |

| GBM_2_AutoML_1_20220719_171824 | 0.089138567 | 0.96055849 | 0.265446264 |

| XGBoost_3_AutoML_1_20220719_171824 | 0.054892909 | 0.59152678 | 0.163465916 |

| GBM_3_AutoML_1_20220719_171824 | 0.034995779 | 0.37711503 | 0.104214137 |

| GBM_4_AutoML_1_20220719_171824 | 0.032231744 | 0.34732974 | 0.095983101 |

| XGBoost_2_AutoML_1_20220719_171824 | 0.016404439 | 0.17677447 | 0.048850875 |

| XGBoost_1_AutoML_1_20220719_171824 | 0.012321778 | 0.13277965 | 0.036693094 |

| GLM_1_AutoML_1_20220719_171824 | 0.003022545 | 0.03257099 | 0.009000855 |

| XRT_1_AutoML_1_20220719_171824 | 0.000000000 | 0.00000000 | 0.000000000 |

| DRF_1_AutoML_1_20220719_171824 | 0.000000000 | 0.00000000 | 0.000000000 |

The table above gives us the variable importance of the metalearner in the ensemble. The AutoML Stacked Ensembles use the default metalearner algorithm (GLM with non-negative weights), so the variable importance of the metalearner is actually the standardized coefficient magnitudes of the GLM.

h2o.varimp_plot(metalearner)

14.1. Generating Predictions Using Leader Model#

We can also generate predictions on a test sample using the leader model object.

pred <- as.matrix(h2o.predict(aml@leader,test_h)) # make prediction using x data from the test sample

head(pred)

|======================================================================| 100%

| predict |

|---|

| 3.028706 |

| 2.533245 |

| 2.823822 |

| 2.470121 |

| 2.776539 |

| 2.678759 |

This allows us to estimate the out-of-sample (test) MSE and the standard error as well.

y_test <- as.matrix(test_h$lwage)

summary(lm((y_test-pred)^2~1))$coef[1:2]

- 0.218083617310276

- 0.0149540081481586

We observe both a lower MSE and a lower standard error compared to our previous results (see here).

h2o.shutdown(prompt = F)